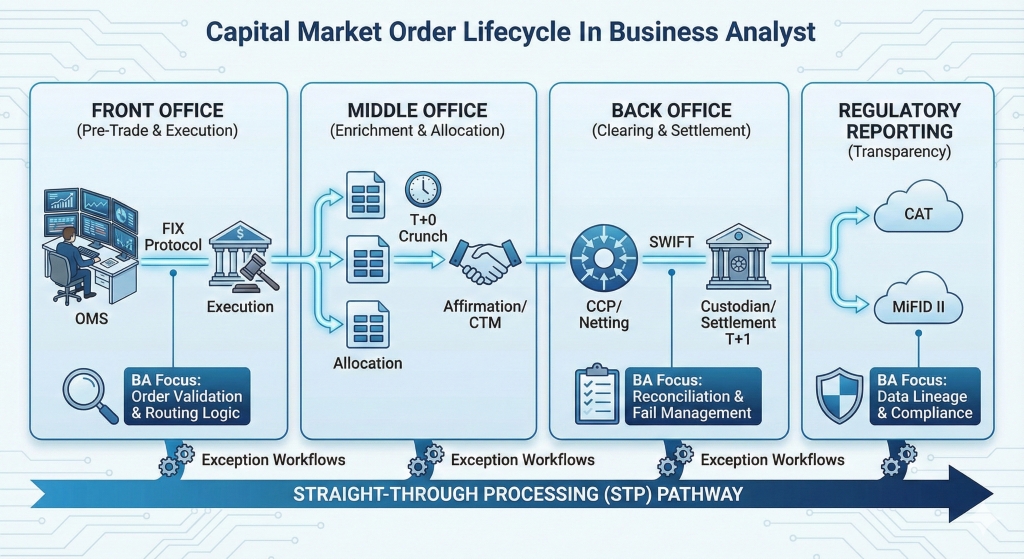

1. Executive Summary for BAs

For a Business Analyst (BA) in Capital Markets, understanding the "happy path" of a trade is elementary. The real value lies in mapping the exceptions, data transformations, and latency sensitivities that occur as an order travels from a Portfolio Manager's blotter to a Custodian’s vault.

This guide dissects the Order Lifecycle (Front-to-Back) with a focus on Straight-Through Processing (STP), protocol mapping (FIX/SWIFT), and the critical impacts of the T+1 Settlement regime.

2. Phase I: The Front Office (Pre-Trade & Execution)

Context: Speed, Accuracy, and Compliance.

2.1 Order Generation & Capture

The lifecycle begins in the Order Management System (OMS) (e.g., Charles River, Aladdin, Eze).

- Trigger: Portfolio Manager (PM) decides to rebalance a fund or take a position.

- BA Requirement Check:

- Compliance Engine: The order must pass pre-trade compliance checks (e.g., Is this stock on the Restricted List? Does this violate the 5% concentration limit?).

- Cash Check: Does the fund have settled cash or available margin?

2.2 Routing & The FIX Protocol

Once validated, the order moves to the Execution Management System (EMS) or is routed directly to a broker/exchange via FIX (Financial Information eXchange) protocol.

- Key Data Mapping (FIX 4.2/4.4/5.0):

Tag 35 (MsgType): D (New Order Single).Tag 54 (Side): 1 (Buy), 2 (Sell).Tag 38 (OrderQty): Quantity.Tag 40 (OrdType): 1 (Market), 2 (Limit).Tag 11 (ClOrdID): Unique Client Order ID (Crucial for BAs to trace orders).

- BA Artifact: Create a Data Dictionary mapping internal OMS fields to outbound FIX Tags.

2.3 Execution

The Broker/Algo executes the trade.

- Inbound Message: The broker sends back an Execution Report (FIX Tag 35=8).

Tag 150 (ExecType): 0 (New), F (Trade/Fill).Tag 39 (OrdStatus): 1 (Partially Filled), 2 (Filled).

- BA Focus: Handling "Partial Fills." If an order for 10,000 shares is filled in 5 chunks of 2,000, does the OMS aggregate them correctly into one "Trade"?

3. Phase II: The Middle Office (Enrichment & Allocation)

Context: The "T+0" Crunch. Under T+1 settlement rules, this phase is now time-critical.

3.1 Trade Capture & Enrichment

The raw execution data flows from Front Office to Middle Office.

- Enrichment: The system appends static data:

- SSIs (Standard Settlement Instructions): Where should the cash/stock be delivered? (e.g., Deliver to JP Morgan, Account X).

- Commission/Fees: Calculating soft dollars, SEC fees, stamp duty.

3.2 Allocation

The PM placed a "block order" for 100,000 shares, but this belongs to 5 different sub-funds.

- Process: The Block Trade is "Allocated" (split) across the 5 funds based on pre-set logic (e.g., Pro-Rata).

- BA Requirement: Ensure the Oasys/CTM (Central Trade Manager) integration supports automated allocation.

3.3 Affirmation & Confirmation

This is the handshake between the Buy-Side (Investment Mgr) and Sell-Side (Broker).

- The Workflow:

- Notice of Execution (NOE): Broker sends trade details.

- Allocation: Buy-side sends allocation details.

- Confirmation: Broker confirms the split.

- Affirmation: Buy-side agrees via a matching utility (e.g., DTCC CTM).

- T+1 Criticality: In the US/Canada markets, affirmation must ideally happen by 9:00 PM ET on Trade Date (T) to ensure settlement. BAs must design workflows that alert operations teams to "Unmatched" trades by 5:00 PM.

4. Phase III: The Back Office (Clearing & Settlement)

Context: Cash Management, Custody, and Reconciliation.

4.1 Clearing (CCP)

For central markets (Equities/Derivatives), a Central Counterparty (CCP) steps in (e.g., NSCC/DTCC).

- Novation: The CCP becomes the buyer to every seller and seller to every buyer.

- Netting: The CCP "nets" the trades to reduce the number of settlements.

- Example: Buy 100 IBM, Sell 50 IBM. Net obligation = Receive 50 IBM.

4.2 Settlement (T+1)

The actual exchange of Cash for Securities.

- Messaging Protocol (SWIFT ISO 15022/20022):

- MT541/MT543: Receive/Deliver against Payment.

- MT548: Settlement Status (Matched/Unmatched/Settled).

- BA Requirement: Gap analysis on SWIFT messages. If a trade fails (fails to settle), how does the system consume the MT548 "Reason Code" (e.g., Lack of Securities)?

4.3 Reconciliation (Recs)

- Cash Rec: Did the cash leave our bank account?

- Position Rec: Does our internal ledger match the Custodian's record?

- BA Tool: Three-Way Rec (Internal System vs. Broker vs. Custodian).

5. Phase IV: Regulatory Reporting

Context: Transparency and Audit Trails.

The trade is legally complete, but not "compliant" until reported.

- CAT (Consolidated Audit Trail) - USA: Every order event (New, Route, Modify, Cancel, Execute) must be reported to FINRA’s CAT database by 8:00 AM the next day.

- MiFID II - Europe: Requires Transaction Reporting (T+1) focusing on "Who made the decision?" (Decision Maker flag) and "Who executed it?" (Algo ID).

- BA Requirement: Data Lineage. You must map the

Trader ID from the Front Office all the way to the regulatory report without truncation.

6. The Business Analyst’s Toolkit

To document this lifecycle effectively, a BA should produce:

- State Transition Diagrams: Showing the life of an order (New $\to$ Partial Fill $\to$ Filled $\to$ Allocated $\to$ Settled $\to$ Archived).

- Field Mapping Matrices: Mapping OMS fields $\to$ FIX Tags $\to$ Swift Tags.

- Exception Workflows: "What happens if the FIX connection drops?" or "What happens if the Client ID is missing?"

- RACI Matrix: Who is responsible for fixing a trade break? (Ops vs. Front Office).

Industry Links for Further Learning

- FIX Trading Community: The global standard for messaging.

- DTCC (Depository Trust & Clearing Corporation): Learn about CTM, T+1, and Settlement.

- SIFMA (Securities Industry and Financial Markets Association): Good for T+1 and regulatory updates.

- Investopedia - Trade Lifecycle: A high-level overview.

International Institute of Business Analysis

· IIBA

BA Blocks

· BA Blocks

· BA Block YouTube Channel

Industry Certification Programs:

CFA(Chartered Financial Analyst)

FRM(Financial Risk Manager)

CAIA(Chartered Alternative Investment Analyst)

CMT(Chartered Market Technician)

PRM(Professional Risk Manager)

CQF(Certificate in Quantitative Finance)

Canadian Securities Institute (CSI)

Quant University LLC

· MachineLearning & AI Risk Certificate Program

ProminentIndustry Software Provider Training:

· SimCorp

· Charles River’sEducational Services

Continuing Education Providers:

University of Toronto School of Continuing Studies

TorontoMetropolitan University - The Chang School of Continuing Education

HarvardUniversity Online Courses

Study of Art and its Markets:

Knowledge of Alternative Investment-Art

· Sotheby'sInstitute of Art

Disclaimer: This blog is for educational and informational purposes only and should not be construed as financial advice.