When most people think of financial economics, they picture grand macroeconomic forces: interest rate decisions, geopolitical shifts, or corporate earnings reports. But beneath the surface of these macro trends lies a hidden, hyper-fast world that dictates how, when, and at what price assets actually change hands.

This is market microstructure—the study of the intricate processes, rules, and technologies that govern the exchange of assets. It is the plumbing of the financial system. If macroeconomics tells us why a stock should be worth $100, market microstructure explains exactly how a buyer and seller finally agree to execute a trade at $100.01.

Understanding market microstructure is no longer just for quants and algorithmic developers; it is essential for anyone trying to grasp modern trading economics. Here is how the microscopic mechanics of the market shape the broader financial ecosystem.

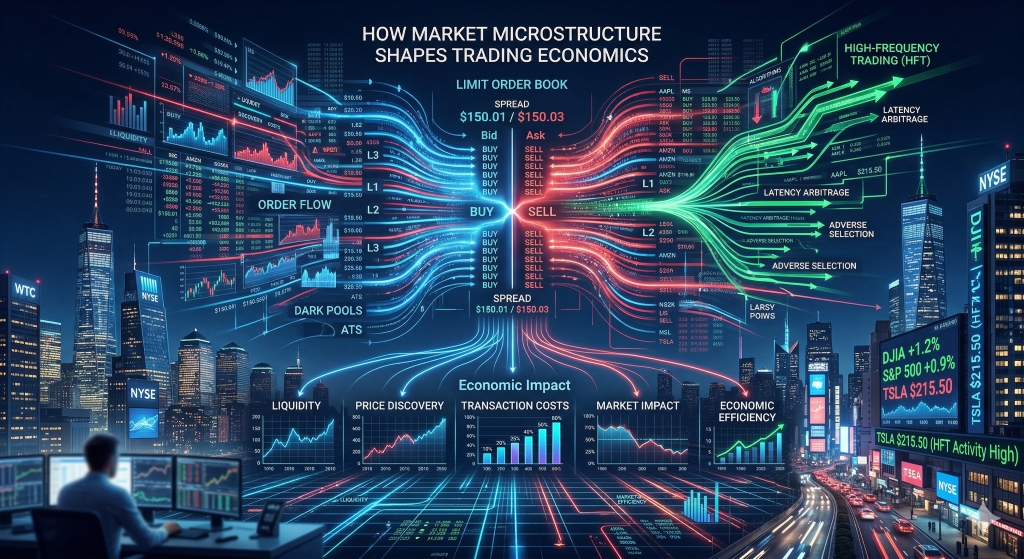

Historically, trading floors were dominated by human market makers shouting over each other. Today, the heartbeat of almost every modern exchange is the Limit Order Book (LOB).

The LOB is an electronic record of all outstanding limit orders (orders to buy or sell at a specific price or better). It is governed by a strict hierarchy:

This system creates a fundamental economic divide between two types of market participants:

Exchanges actively manipulate these economics through Maker-Taker pricing models, often paying rebates to Makers (to attract liquidity) and charging fees to Takers (who consume it). This micro-level fee structure dictates the behavior of algorithmic trading firms worldwide.

Market microstructure teaches us that liquidity isn't just about volume; it's about the cost of trading quickly.

The difference between the highest price a buyer is willing to pay (the bid) and the lowest price a seller is willing to accept (the ask) is the spread. The spread is a direct measure of market friction. In highly liquid markets (like large-cap tech stocks or major forex pairs), the spread is razor-thin. In illiquid markets, the spread widens to compensate market makers for the risk of holding an asset they might not easily sell.

How does new information get baked into an asset's price? Through order flow. When a positive earnings report drops, algorithms don't simply "update" the price. Instead, a wave of buy orders floods the market, eating through the existing "ask" orders in the LOB until the price settles at a new, higher equilibrium. This mechanical consumption of liquidity is the process of price discovery.

You cannot discuss modern microstructure without addressing the speed of light. Because time priority rules the Limit Order Book, being a microsecond (one-millionth of a second) faster than your competitor is an economic moat.

HFT firms invest heavily in microwave towers, custom FPGA chips, and co-location (placing their servers in the exact same building as the exchange's matching engine).

The Economics of Speed:

While HFT has compressed bid-ask spreads (benefiting retail investors), it has also introduced "phantom liquidity"—orders that disappear the millisecond the market shifts, leading to phenomena like the 2010 Flash Crash.

In the early 2000s, regulations like Reg NMS in the US and later MiFID II in Europe were introduced to foster competition among exchanges. They succeeded, but they also fragmented the market. Today, a stock like Apple doesn't just trade on the NASDAQ; it trades across dozens of lit exchanges and alternative trading systems (ATS).

To avoid the market impact of massive institutional trades—where a large buy order signals to the market that a whale is buying, driving the price up before the order finishes—institutions turned to Dark Pools.

Dark pools are private exchanges where order books are not visible to the public. Trades are executed anonymously, and prices are usually derived from the midpoint of the public lit markets. The economic trade-off is clear: participants sacrifice price discovery and guaranteed execution for reduced market impact and privacy.

Market microstructure is currently undergoing its next evolution. Machine learning models are moving beyond simple statistical arbitrage to deep reinforcement learning, predicting short-term order book imbalances with terrifying accuracy.

Simultaneously, Decentralized Finance (DeFi) is pioneering entirely new microstructure models, such as Automated Market Makers (AMMs) used by decentralized exchanges like Uniswap. Instead of an LOB, AMMs use mathematical formulas (like x * y = k) to price assets in liquidity pools, stripping away the traditional middleman entirely.

Understanding these mechanics proves that prices are not perfectly rational reflections of intrinsic value; they are the messy, fascinating result of millions of micro-interactions governed by speed, rules, and silicon.

Here are some authoritative resources you can link to for readers who want to dive deeper into the professional and academic sides of market microstructure:

BA Blocks

Industry Certification Programs:

CFA(Chartered Financial Analyst)

FRM(Financial Risk Manager)

CAIA(Chartered Alternative Investment Analyst)

CMT(Chartered Market Technician)

PRM(Professional Risk Manager)

CQF(Certificate in Quantitative Finance)

Canadian Securities Institute (CSI)

Quant University LLC

· MachineLearning & AI Risk Certificate Program

ProminentIndustry Software Provider Training:

· SimCorp

· Charles River’sEducational Services

Continuing Education Providers:

University of Toronto School of Continuing Studies

TorontoMetropolitan University - The Chang School of Continuing Education

HarvardUniversity Online Courses

Study of Art and its Markets:

Knowledge of Alternative Investment-Art

Disclaimer: This blog is for educational and informational purposes only and should not be construed as financial advice.