For over a decade following the 2008 financial crisis, the global economy operated under a "free money" regime. Capital was abundant, risk was cheap, and "growth at all costs" was the mantra. As we navigate 2026, that era feels like ancient history. We have entered a period of rate normalization, where the cost of capital is no longer a rounding error but the primary filter through which every deal, IPO, and infrastructure project must pass.

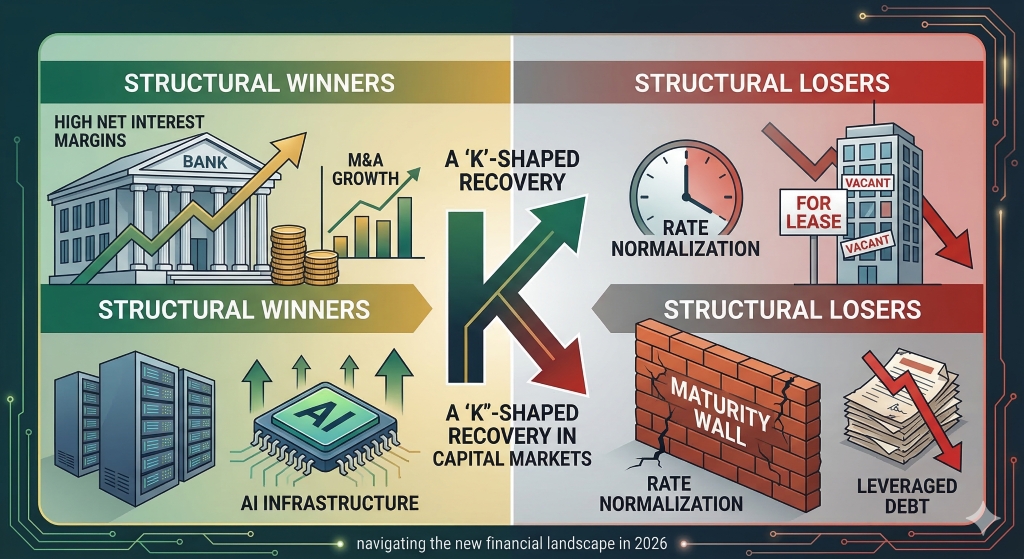

The transition to this "higher-for-longer" environment has created a K-shaped recovery in the capital markets. On one side, structural winners are thriving by leveraging high-quality balance sheets and the AI-driven capex boom. On the other, losers are being winnowed out as the "maturity wall" finally hits home.

As of March 2026, the Federal Reserve has stabilized rates in the $3.25\%–3.50\%$ range. While significantly lower than the 2023 peaks, this is still worlds away from the $0\%$ floor of the previous decade. Inflation has settled near $3\%$, kept "sticky" by resilient labor markets and the massive energy requirements of the AI revolution.

In this environment, liquidity is no longer a tide that lifts all boats; it is a laser that spotlights quality.

While high rates initially sparked fears of banking instability, the 2026 landscape tells a different story. Large, diversified banks are the primary beneficiaries of a steepening yield curve. They are paying less on short-term deposits while reaping higher yields on long-term corporate debt and 30-year mortgages.

The retreat of traditional banks from riskier lending has handed a permanent crown to Private Credit. Institutional investors are flocking to this asset class for its floating-rate nature, which provides a natural hedge against persistent inflation.

In the equity markets, the "Magnificent Seven" era has evolved into the "Infrastructure Three": energy, data centers, and semiconductors. Companies with "fortress balance sheets" that can self-fund massive AI capex are outperforming small-caps that are still choking on high borrowing costs.

The most visible loser remains the office sector. Between 2026 and 2029, over $2$ trillion in CRE debt is set to mature. Most of these loans were inked at near-zero rates.

The era of "multiple expansion" (buying a company and selling it for more simply because the market grew) is dead.

Companies with "floating-rate-only" debt structures are the "canaries in the coal mine." As rates stay elevated, the percentage of revenue going toward debt service is ballooning, leading to a rise in idiosyncratic defaults across the retail and manufacturing sectors.

BA Blocks

Industry Certification Programs:

CFA(Chartered Financial Analyst)

FRM(Financial Risk Manager)

CAIA(Chartered Alternative Investment Analyst)

CMT(Chartered Market Technician)

PRM(Professional Risk Manager)

CQF(Certificate in Quantitative Finance)

Canadian Securities Institute (CSI)

Quant University LLC

· MachineLearning & AI Risk Certificate Program

ProminentIndustry Software Provider Training:

· SimCorp

· Charles River’sEducational Services

Continuing Education Providers:

University of Toronto School of Continuing Studies

TorontoMetropolitan University - The Chang School of Continuing Education

HarvardUniversity Online Courses

Study of Art and its Markets:

Knowledge of Alternative Investment-Art

Disclaimer: This blog is for educational and informational purposes only and should not be construed as financial advice.